May 2023 Market Insights

11-County Metro Denver Area

May's housing market demonstrates resilience amid economic uncertainty, showcasing stability in terms of key metrics. This time of year typically witnesses increased market activity as more buyers and sellers participate, leading to a surge in inventory and prices. This phenomenon is commonly referred to as the spring selling season. However, the current spring season seems to lack the usual vigor, with both new listings and closings occurring at a slower pace compared to previous years. As the possibility of a recession looms, prospective buyers and sellers must carefully consider various factors when navigating the local housing market.

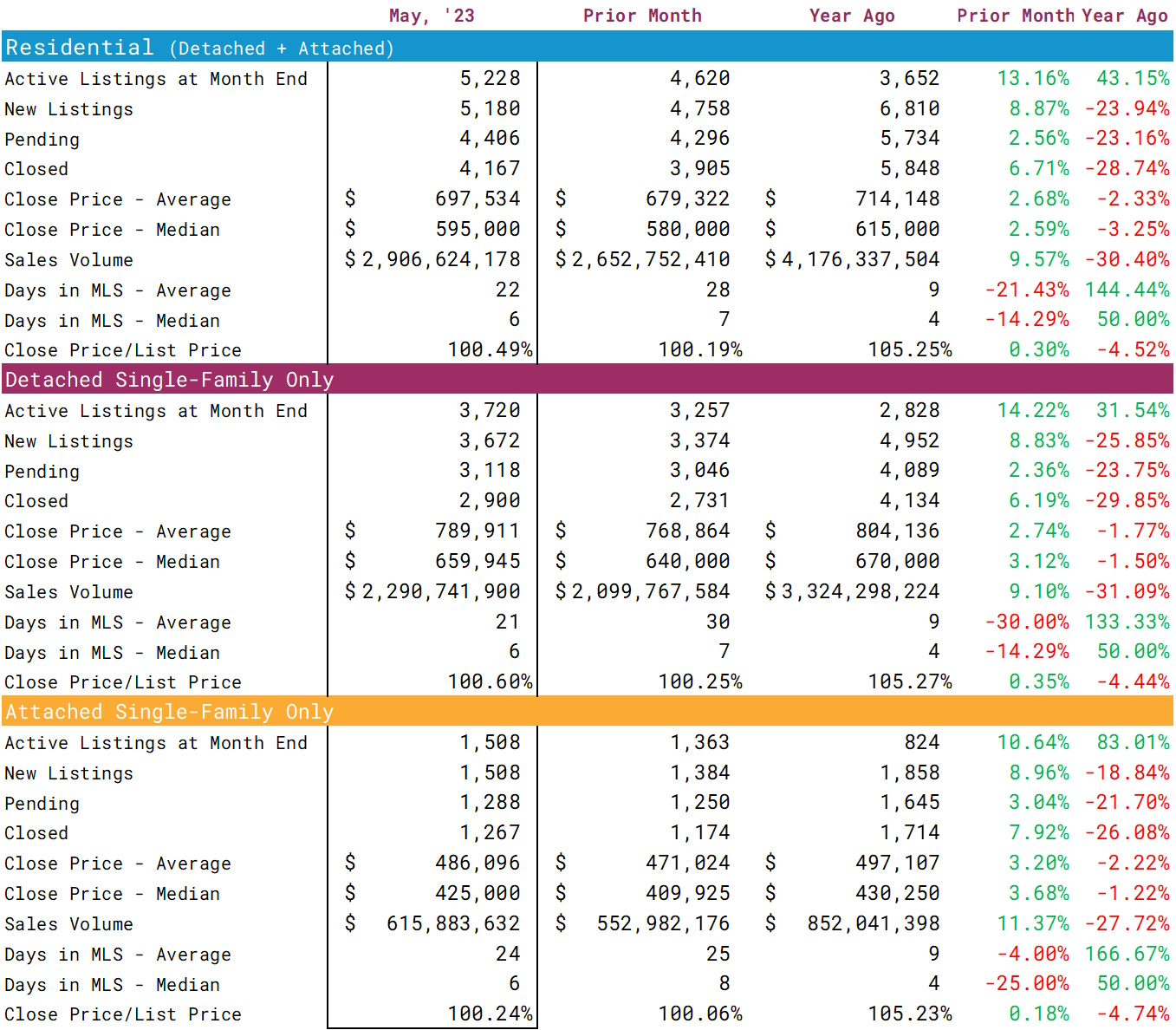

In May, the average home price reached $697,534, reflecting a 2.68 percent increase from April's average of $679,322. This positive trend is encouraging, considering that the average change from April to May typically hovers around 1.42 percent. The median price also follows a similar pattern, rising by 2.59 percent compared to April. However, it is important to note that prices are currently below the figures recorded in May of the previous year, amounting to a 2.33 percent decrease from the corresponding period.

Overall, the housing market is experiencing approximately 25 percent less activity compared to the previous year. Consequently, there is a reduced number of new listings, sales, and closings. Year-to-date, there have been 6,069 fewer new listings and 5,357 fewer closings compared to the same period last year. These figures highlight significant missed opportunities for both buyers and sellers.

It is worth mentioning the concept of "shadow demand," which may be unfamiliar to some individuals. Shadow demand refers to an influential effect on the market that cannot be identified within the available data. We witnessed a similar phenomenon during the post-2008 mortgage market collapse, characterized by the existence of "shadow inventory." This term denoted the substantial number of distressed properties that lenders withheld from the general market. If these properties had been released to the public, it would have significantly altered the course of the recovery.

Applying this concept to the current situation, it is evident that shadow demand exists. The Denver metro area has long grappled with inadequate housing supply to accommodate the influx of residents over the past decade. Consequently, Denver has emerged as one of the nation's leading housing markets in terms of price growth. In the second quarter of 2022, the rapid increase in mortgage rates due to inflationary pressures resulting from government spending adversely affected buyer affordability. Many prospective buyers are likely waiting for improved conditions before entering the market.

As of the end of May, there were 5,228 available homes for sale, marking a 13.16 percent increase from April and a substantial 43.15 percent increase from April 2022. Among the available homes, 40.9 percent have reduced their asking prices, with an average reduction of $69,309. Interestingly, in May 2006, the market reached its record high with 30,457 available homes for sale. The last May to exceed 10,000 listings was in 2012.

Lastly, let's explore some noteworthy trends observed in the rental segment of the housing market. In the single-family category, the average number of days on the market decreased to 27 days in May, down from 38 days in April. The multi-family segment experienced a slightly less significant decline, with an average of 29 days on the market compared to 34 days in April. Additionally, the median rent for a two-bedroom single-family home stands at $2,095, representing a 4.75 percent increase compared to May 2022. It appears that the rental market is performing stronger than the re-sale side.