July 2023's Housing Update

11-County Metro Denver Area

By the numbers, July's local housing market shows limited growth, presenting mixed signals that point to potential uncertainty ahead. The Federal Reserve believes that continued tightening of monetary policy may be necessary, leading to higher mortgage rates in the coming months and reducing affordable housing options. Consequently, buyers are adapting their behaviors, becoming bargain hunters seeking value. However, there are positive aspects as well, with home prices starting to stabilize. Be mindful when listening to those national stories as metro Denver tends to run counter to national housing trends.

Let's start by examining inventory. At the end of July, there were 6,299 active listings, representing a 14.43 percent decrease compared to the previous year. While this year's inventory is lower, it is not critically low. In July 2021, we experienced a record low with only 4,056 homes available for sale. Additionally, we keep track of how many of those homes have reduced prices, and currently, 45.4 percent have reduced prices, up from 34.0 percent last year.

The market continues to face challenges due to a lack of new listings. This phenomenon, referred to as the "Golden Handcuffs," sees homeowners deciding not to sell their homes due to the gap between their low mortgage rates and the current market rates. In July, there were only 4,773 new listings, a significant 24.76 percent decrease from the previous year. Fewer homes available for sale ultimately lead to fewer home sales.

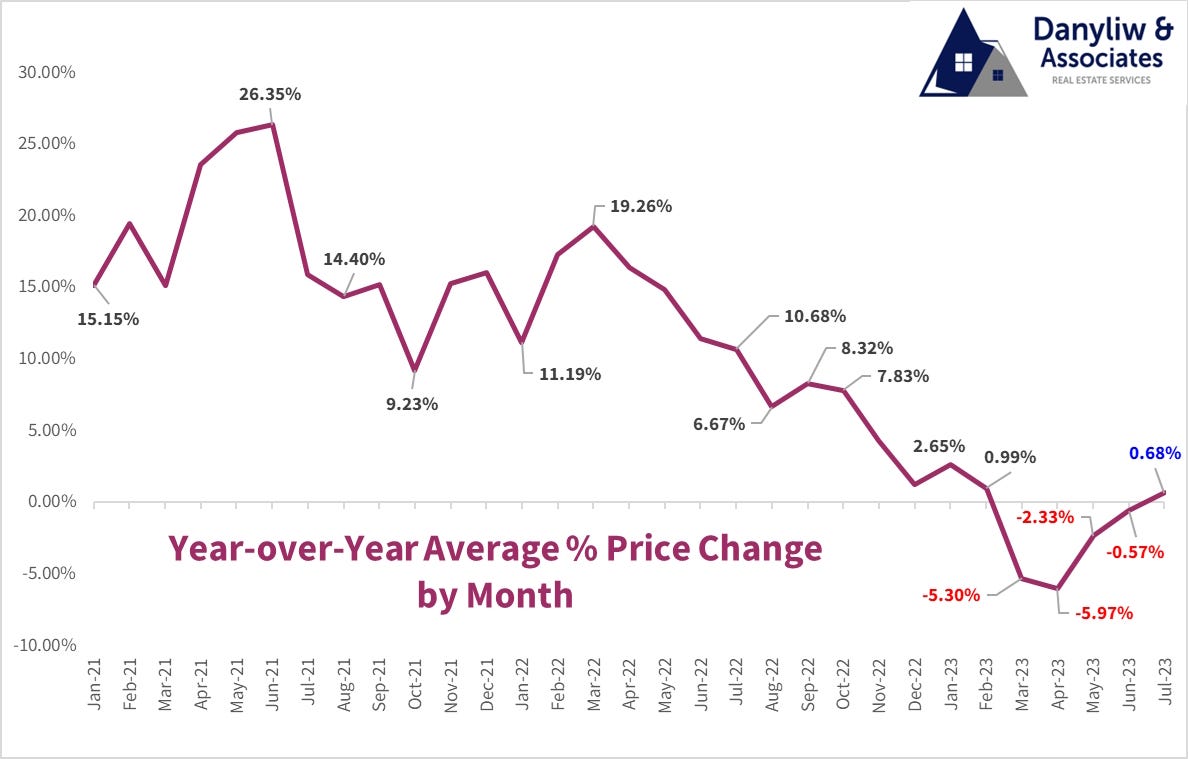

In terms of pricing, the average closed price dropped 2.43 percent from last month, which is not alarming news. Our housing market follows seasonal cycles, with mid-summer being the peak. Historically, we typically see an average price drop of 2.61 percent the following month after the peak. Therefore, this July's drop of 2.43 percent is relatively positive. Moreover, the average closed price in July was $693,449, marking a 0.68 percent increase compared to last July. This represents the first year-over-year price increase since February of this year.

Seller paid concessions are becoming more common, with 48 percent of closed transactions this year involving seller concessions, compared to 29.2 percent last year. The average concession was $7,295, with the largest single concession reaching a significant $108,227. This statistic serves as an indicator of market strength and is valuable information for sellers before listing their homes for sale.

Higher mortgage rates are significantly impacting the market, affecting both buyers and sellers differently. Prospective sellers are hesitant to enter the market, while buyers find it increasingly challenging to afford a home. Dr. Lawrence Yun, NAR's chief economist, updated his forecast, anticipating a drop in rates to 6 percent by year-end. However, some caution is warranted, as I am not as optimistic at this point. Nonetheless, deals are still being made, and prices have not experienced the collapse that many had predicted.