April's Market Insights

11-County Metro Denver Area

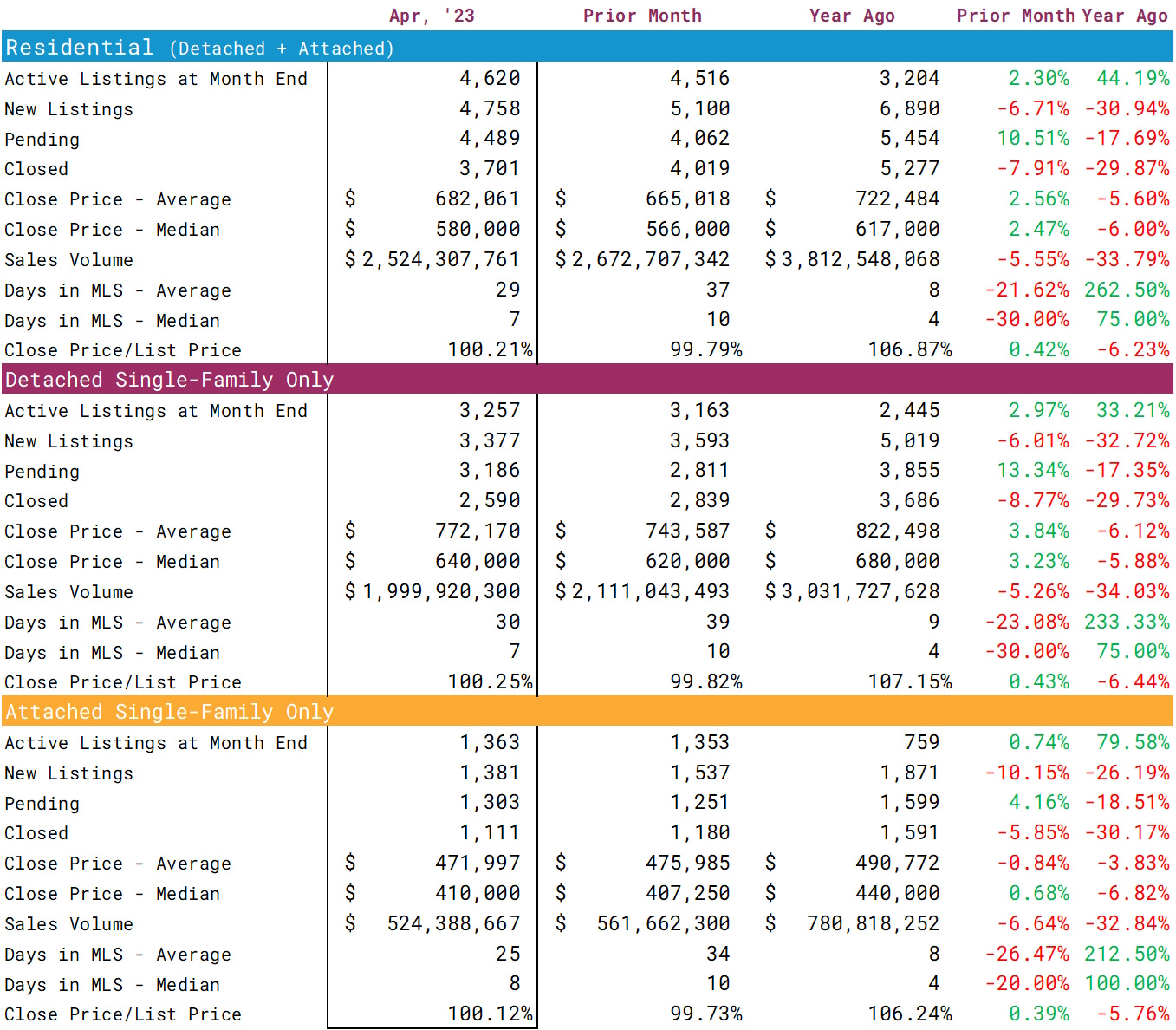

Let us begin by examining the supply side of the market. The inventory of unsold homes has increased to 4,620, or 2.3 percent from the preceding month's 4,516. While a rise in inventory is expected during the spring, April's increase fell short of the anticipated seasonal rise of 10.41 percent. The fluctuation of inventory is driven by the influx and outflow of homes in the market.

New listings for April decreased to 4,758, or 6.71 percent from the previous month. Typically, we expect an increase of 8.45 percent during this season. However, homeowners may be hesitant to sell due to higher mortgage rates and general economic uncertainty. Most homeowners have a rate at or below 3.5 percent, which translates to a lower monthly payment. This discrepancy in rates could hinder the number of new listings entering the market in the foreseeable future.

On the other side of the equation are the listings being taken off the market. Pending listings are also falling behind our seasonal norms. In April, 4,489 listings shifted from active to pending status, marking a 10.51 percent increase from March but below the seasonal expectation of 13.91 percent.

In April, the average number of days a property spent on the market dropped to 29, compared to 37 days in March and 48 days in February. To provide further context, in April 2022, the average number of days was 8. Although most properties are taking longer to sell, they are being sold for more than the asking price. In April, homes closed for 100.21 percent of the asking price, marking the first time since July 2022 that this figure has surpassed 100 percent.

The average closed price for April is $682,061, which is a 2.56 percent increase from March but a 5.6 percent decrease from April 2022. I am keeping a close eye on this year-over-year percentage change since I had previously predicted that prices would fall between 4 to 6 percent for the year, and so far, the market appears to be on track with this projection. The median price is $580,000, which is up by 2.47 percent from March but down by 6.0 percent from last year.

Ultimately, the interplay between supply and demand will dictate the direction of prices. Buyer demand has slowed, but seller supply has slowed even more. This dynamic will keep inventory on the low side, and as a result, prices should remain stable. Overall, the housing market is resilient, and buyers and sellers are adaptable to change. However, we need the volatility of mortgage rates to ease before the housing market can experience growth once again.